1.1 The environmental accounting: brief overview

Environmental accounting stands for all the systems that allow detecting, organising, managing and communicating environmental information and data, these last ones expressed in monetary and physic units. The idiom “environmental accounting” indicates the reorganizing of the accounting systems by including new cost categories and reclassifying of traditional categories as to offer trustworthy and useful information for the control, management and communication activities. It should be able to offer to the public administration the necessary information for pointing out the environmental critical situations and for the efficiency control of the carried out policy.

The environmental accounting is part of an internationally accepted set of principles. The 1992 Rio de Janeiro UN Conference on the environment put a milestone by approving the 21 Agenda for the sustainable development, stipulating –among actions to be taken – the environmental accounting practice in all countries.

The European Commission has many times underlined in the V and VI Action Program for the environment, the importance of adopting environmental accounting instruments at all levels of administration, in order to the integrate the information contained in the traditional economical-financial programming and balance documents and thus adequately support the public decision process. On March the 2nd, European Council Recommendation states the following: “The adoption of an environmental accounting system at all levels of the government would allow the political decision makers to report to the administered communities on the environmental results and carried out policies, based on trustworthy data and constantly updated information on the environmental state, to include the “environment” variable in the public decision procedure at all governmental levels and finally to increase the transparency on the results of the public bodies policies on the environment”.

Initially, the environmental accounting functions were:

1. Measuring and evaluating the state and the variations of the natural environment and of the anthropic activities impacts on it;

2. Accounting and evaluating the monetary and financial fluxes referred to the natural common goods use and to the man-environment interaction.

The first methodological profile has brought up physic accounts expressed in physic nature measuring units; the second methodological profile regards the monetary accounts.

The local application of the environmental accounting and environmental balance has out-spotted other two functions:

1. The information and statistic one;

2. The governmental one, connecting the data, physic and monetary indexes “account” to the environmental policies formulation, programming and control (the “statement of accounts” of the obtained results).

Some of the most internationally recognized methods are briefly described in the following boxes.

Focus: The CLEAR method

CLEAR (City and Local Environmental Accounting and Reporting) is nowadays the most diffused environmental accounting system specific for the local administrations in Italy. It was developed beginning with 2001 through a Life project by the Ferrara City Hall and other 17 local authorities. It is a method thought for the local public administrations and deciding authorities in order to get environmental politics quantifiable and evaluate their impacts, efficiency and results. It is a structured method defining the accounting principles and guaranteeing the environmental balance development, contents, and structure. It stipulates the annual environmental balance (estimated and final) based on a political- Authority procedure aligned to the ordinary balance sheet.

The method is based on the environmental data collecting and management “accounting” (counting and accounting) conceptual evolution into “accountability” (reporting the accounts), that indicates the putting up of a responsibility system for clarifying the existing relationships between decisions, activities and control parameters of the outcomes (indexes).

The environmental balance is structurally based on the legal competencies of the authority and contains the pursued strategic tasks and environmental politics to which physic indexes (Physic accounts) and economic ones (Environmental expenses) are associated in order to evaluate the proceeding of the activities put into practice.

The process is developing according to the following steps:

‣ Defining the authority’s environmental politics starting from analysing the environmental politics, programs and tasks explanatory documentation;

‣ Developing the accounting system. Identifying the fields for reporting, defining the measurement and control parameters (physical and monetary indexes) for the policies’ effects assessment; gathering of indexes values by installing systematic gathering procedure of relevant information;

‣ Reporting. Communicating the authority achievements of tasks through the report release, that is a synthesis of the environmental accounting system (Final environmental balance).

The involving of the stakeholders is foreseen all along the process so that the system might include their expectations and the accounting system might be shared. The process’s circle closes with redefining the policies based on the outcomes and the authority’s performance (estimated environmental balance).

The reference standards

The CLEAR method was defined based on some internationally accepted standards and methodologies. The main reference points regard the implementation process (AA1000), the reporting (GRI) and the environmental expense (SERIEE-EPEA). The CLEAR method has reprocessed these methodologies principles and criteria and adapted them to the needs of the local authorities’ environmental policy management and reporting.

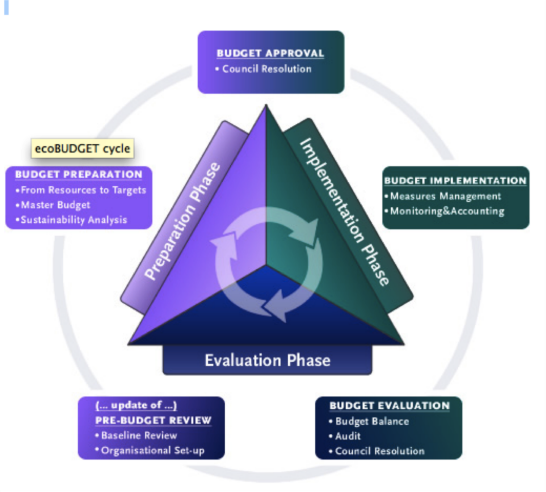

Focus: ECObudget

EcoBUDGET is the environmental management system developed with local governments in mind. Based on the physical description of use and consumption of natural resources within the municipal territory, ecoBudget allows local governments to present tangible achievements of their sustainability oriented polices to the greater public.

Without assigning monetary value to the environment, ecoBudget applies principles and routines of financial budgeting to the management of natural resources.

Unlike other environmental management systems, ecoBudget is concerned with the management of natural resources within the municipal territory and community as a whole.

ecoBudget is unique in its requirement that quantitative long-term and annual targets must be ratified by the city council. Therefore it influences the direction of local environment policies.

The ecoBUDGET cycle is a 5-step approach that mirrors the three phases of the municipal financial budgeting cycle including budget planning (i.e. the preparation of an environmental budget), budget spending (i.e. the implementation of planned measures to meet the budget), and budget balancing (i.e. balancing the annual environmental accounts). These are familiar to decision makers so that environmental budgeting becomes as much a part of local authority routines as financial budgeting.

• Phase 1 - Budget preparation and approval

Based on the current environmental situation in the municipality, departments identify the natural resources they require for budget planning, identify budget priorities, set targets and prepare the environmental master budget which is presented to the Council for approval.

• Phase 2 - Budget implementation

Following the Council's approval, programmes and measures are undertaken to meet the environmental targets. The implementation measures and compliance with the targets are monitored and accounted for.

• Phase 3 - Budget balancing

At the end of the budget year, just as with financial budgeting, a statement of the environmental accounts is prepared - the (environmental) Budget Balance.

Focus: The Global reporting initiative

The Global Reporting Initiative (GRI) is a multi-stakeholder international process that aims to develop and diffuse the guidelines for creating sustainability balance sheets. The guidelines regard organizations governmental, non-governmental, companies) that want to report the economical, environmental and social aspects of their activity, products and services. In particular, they:

• Present the balance-sheets’ basic principles and specific content in order to guide their preparation;

• Assist the organizations in presenting their economic, environmental and social performance in a balance and reasonable way;

• Promote the sustainability balance-sheets comparison, still taking into account the practical aspects related to information diffusion between different organizations;

• Support the benchmarking and the performance sustainability’s appreciation with regard to codes, standards and voluntary initiatives;

• Are stakeholders’ engagements facilitating instruments.

The guidelines published in 2002 were mainly developed for companies, but other organizations like governmental agencies and no-profit organizations can make use of them. A supplement for the public administration was recently released. Its purpose is to fill the gap in the public domain reporting instruments and give a significant contribution to the internationally emerging sustainability reporting system. Eurostat, the European Statistics Institute has defined the Seriee system (Système Européen de Rassemblement de la Information Economique sur l’Environnement) within which EPEA (Environmental Protection Expenditure Account), a specific environmental protection expense “satellite” account, was encoded. EPEA is the European satellite account of the environmental protection expense targeted for registering the economical transactions concluded by the whole of the economical operators and regarding the environmental protection function. The established methodology for setting the items regarding Public Administration’s expense for environmental protection is based on the analysis of expense basic units (expense items) for Final balances of various public authorities and their classification by a shared scheme (CEPA). A second satellite account (RUMEA) for the use and management of natural resources is now being defined.